Bitget UEX Daily |US Commerce Secretary Urges Korean Memory Giants to Expand US Production; Warsh Forms Expert Team to Review Monetary Policy Framework; SK Hynix Set to List on US Markets

Bitget2026/07/10 01:26

Bitget2026/07/10 01:26

I. Hot News Highlights

Federal Reserve Updates

Fed Chair Warsh Forms External Expert Teams for Comprehensive Review of Monetary Policy Framework

- Kevin Warsh announced the establishment of five independent working groups (Inflation, Balance Sheet, Employment, Data, and Communications), led by renowned economists and former central bank officials (including Chetty, Andreessen, Mankiw, etc.). The goal is to assess whether tools, analytical methods, and the overall framework are suited to rapid economic transformation.

- The groups will submit fact-based analyses to the FOMC and reaffirm the Fed’s “unwavering commitment” to price stability and maximum employment.

- Market impact: The review signals that the Fed is proactively adapting to AI and structural changes, strengthening near-term expectations for policy flexibility and helping stabilize interest rate path pricing while reducing excessive hawkish concerns.

International Commodities

US-Iran Conflict Escalates Again as Trump Declares Ceasefire Over and Restarts Strikes

- Trump stated that the ceasefire has ended due to Iran’s continued attacks on ships in the Strait of Hormuz. US forces struck at least 170 Iranian military targets within 48 hours, with Iran retaliating against US bases. Israel shared intelligence on a “new Iranian plot to assassinate Trump,” prompting a precautionary aircraft change after the NATO summit.

- Pakistan and Qatar continue mediation efforts. US officials say technical negotiations remain ongoing and Iran must never acquire nuclear weapons. Some Republican lawmakers worry rising oil prices could hurt midterm election prospects.

- Market impact: Geopolitical risks temporarily boosted oil volatility and safe-haven demand, but actual supply disruption has been limited. The pullback in oil prices shows markets are cooling expectations of rapid escalation, providing staged support for precious metals.

Macroeconomic Policy

US Temporarily Exempts Commercial Aircraft and Jet Parts from Tariffs; OpenAI Officially Launches GPT-5.6 After Government Consultations

- After completing the investigation, the Commerce Department decided not to impose tariffs for now and instead instructed negotiations with trading partners. Trump may take further action if no effective agreement is reached within 180 days. OpenAI released the Sol/Terra/Luna model series after consultations with Lutnick, Bessent and other officials, rolling out access in stages to the public.

- Former Fed Chair Ben Bernanke joined Anthropic’s Long-Term Benefit Trust to oversee AI’s social impact and board appointments.

- Market impact: The tariff delay eases pressure on the aviation supply chain. AI regulatory collaboration signals enhance long-term certainty for large model companies while highlighting deeper government involvement in AI infrastructure.

II. Market Recap

Commodities Forex Performance (Real-time Update)

- Spot Gold: $4,120/oz, -0.09%

- Spot Silver: $60.02/oz, +0.14%

- WTI Crude: $71.95/bbl, -0.18%

- Brent Crude: $76.00/bbl, -0.24%

- US Dollar Index (DXY): 100.819, -0.14%

Driving Factor Analysis: Despite the renewed escalation of US-Iran tensions (Trump restarting strikes, aircraft change, and assassination plot intelligence), crude oil only posted a mild decline. Analysts generally believe the market has fully digested the risk premium—actual supply impact remains limited, combined with soft global demand and mediation efforts by Pakistan and Qatar. Goldman Sachs and other institutions had previously lowered their 2026 oil price centers; current price action confirms a “controlled conflict” narrative. Gold edged lower while silver rose slightly, showing divergence: safe-haven buying was offset by strength in US tech stocks and rising risk appetite, while silver benefited from industrial demand support. MUFG and other analysts note that Fed Chair Warsh’s framework review and FOMC minutes reveal policy divisions, with higher-for-longer expectations capping upside for precious metals. The dollar index softened in tandem, reflecting the dominance of risk-asset rebound. The overall asset linkage logic is clear—geopolitical disturbance persists, but macro liquidity and institutional consensus on “limited escalation” are driving short-term pricing, with oil under pressure and precious metals remaining range-bound.

Cryptocurrency Performance

- BTC: $63,100, +1.5% (24h)

- ETH: $1,744, +0.25% (24h)

- Total Crypto Market Cap: $2.17 trillion, +approx. 1.0% (24h)

- Market Liquidations: 24h total liquidations ≈ $175 million (longs ≈ $67 million, shorts ≈ $108 million)

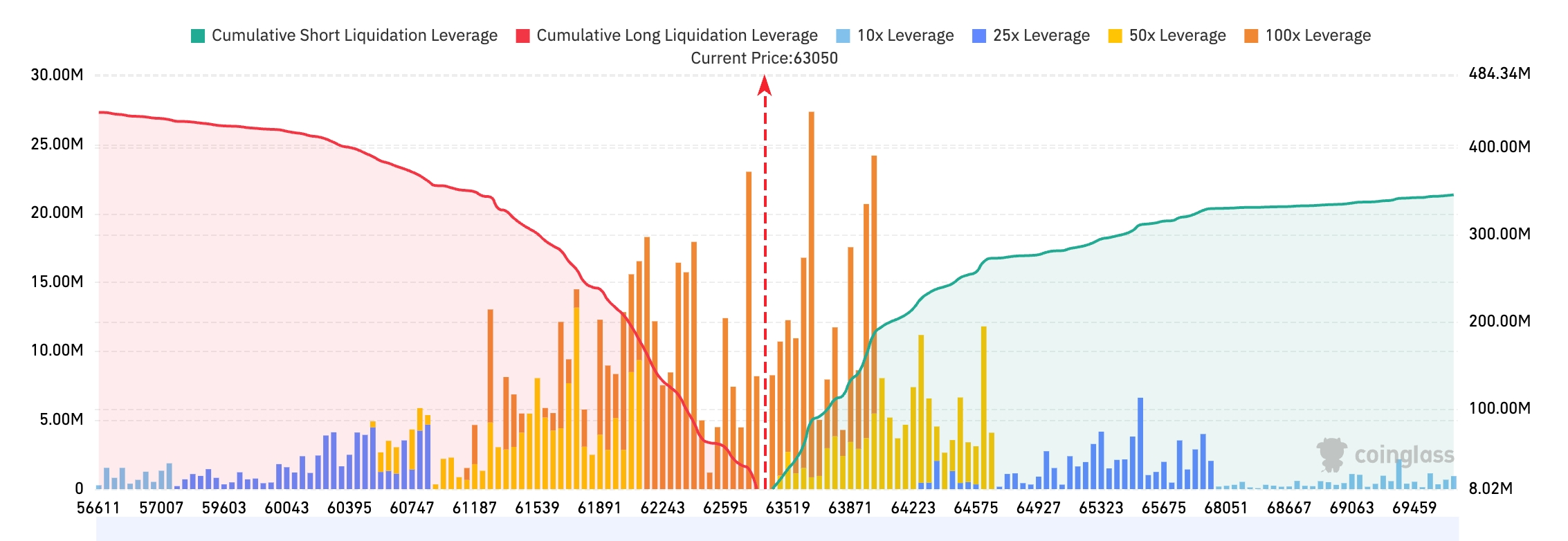

- Bitget BTC/USDT Liquidation Map: Current BTC price around $63,050. Significant short liquidations clustered in the $63,500–$64,500 zone, with densest leverage between $63,800–$64,000. A breakout could trigger a short-squeeze cascade. Clear long liquidation bands exist at $62,000–$62,800, but cumulative size below is weaker than above—short-term liquidation pressure still favors the upside.

- Spot ETF Net Flows: BTC spot ETFs recorded a net outflow of $15 million yesterday (current 24h dynamic also -$15 million)

Driving Factor Analysis BTC showed relative strength while ETH stayed flat and total market cap recovered modestly, reflecting resilient risk appetite amid geopolitical noise. Yesterday’s small ETF outflow and controllable liquidation size (with shorts dominating) indicate that the market’s deleveraging phase has largely completed. Macro support from the Fed framework review and strong tech stocks is present, but the oil pullback and stable dollar limit aggressive upside. Overall trend is range-bound recovery; BTC’s outperformance versus ETH continues the “institutional preference for large-cap coins” pattern. Technical focus remains on the release of overhead liquidation pressure.

US Equity Index Performance

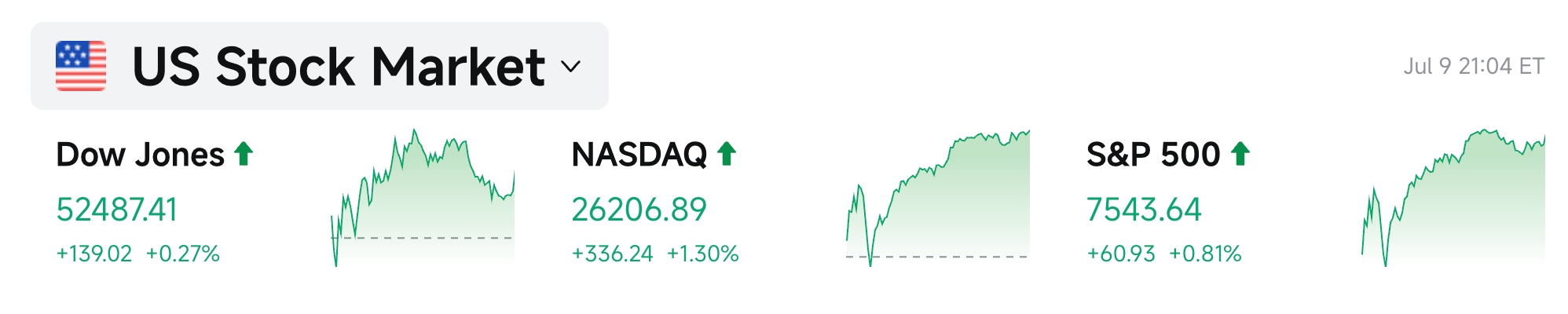

- Dow Jones: 52,487.41 (+0.27%), continued mild gains

- SP 500: 7,543.64 (+0.81%), broad-based steady advance

- Nasdaq: 26,206.89 (+1.30%), led by tech and chip sectors

Tech Giants Performance

- NVDA: ≈$203.50, -0.8%

- AAPL: ≈$316.00, +0.4%

- MSFT: ≈$392.00, +1.3%

- GOOGL: ≈$357.00, -1.4%

- AMZN: ≈$245.00, +0.4%

- META: ≈$615.00, +4%

- TSLA: ≈$407.00, +3.2%

- SPCX: $152, +2.6%

- MU: $991.64, +4.52%

Performance Summary Driving Analysis: The tech sector advanced overall but with clear divergence. Memory and AI infrastructure names (MU, AMD, AVGO) led gains, benefiting from Commerce Secretary Lutnick’s call for Korean firms to expand US production and Micron’s $250 billion investment plan. META surged on Zuckerberg’s denial of excess compute capacity and emphasis on the commercial potential of a cloud business. TSLA was lifted by Optimus production guidance. NVDA pulled back modestly on valuation digestion and competition concerns, while GOOGL faced pressure from company-specific issues. Drivers were highly differentiated—policy and capacity localization favored memory stocks, while company-specific strategic narratives supported META and TSLA—rather than a uniform “AI optimism” theme.

Sector Movers

Memory Chip Sector +over 3%

- Representative stocks: Micron (MU) +4.52%, AMD +nearly 6%

- Drivers: Commerce Secretary Lutnick publicly urged SK Hynix and Samsung to expand US memory production, combined with Micron’s major upward revision of domestic investment, easing AI HBM/memory shortage expectations and attracting rapid inflows.

Semiconductor Equipment +approx. 2%

- Representative stocks: Broadcom +over 3%

- Drivers: Renewed confidence in the sustainability of AI capex, boosted by the imminent SK Hynix IPO.

III. In-Depth US Stock Analysis

1. SK Hynix – Nasdaq Secondary Listing Launch

Event Overview: SK Hynix priced its ADRs at $149 per share, raising approximately $26.5 billion (slightly reduced from the earlier $28–29 billion target). The offering was more than 7x oversubscribed, underscoring strong institutional demand for AI memory. Lead underwriters are Bank of America, Citigroup, Goldman Sachs, and J.P. Morgan, with total commissions expected to exceed $140 million. Shares begin trading on July 10 under the when-issued symbol SKHYV and convert to regular-way trading as SKHY on July 13. Concurrently, Commerce Secretary Lutnick publicly urged SK Hynix and Samsung to expand US memory production to ease global AI component shortages, stating he wants to “bring their competitors to the US to build factories,” even if Micron’s CEO may not welcome it. Proceeds will primarily fund new factories and equipment to meet surging HBM demand.

Market Interpretation: Wall Street views this as one of the largest foreign-company IPOs in history (second only to SpaceX). Institutions see it as a core AI supply-chain name whose valuation could re-rate higher with US liquidity and analyst coverage (it previously traded at a discount in Korea). Multiple banks note that heavy oversubscription and high commissions reflect long-term optimism on HBM supply-demand tightness, though some warn the large listing could force institutions to sell Micron or Nvidia to fund allocations, creating short-term sector volatility. Lutnick’s comments are interpreted as acceleration of the US “chip reshoring + ally capacity-sharing” policy—positive for global memory leaders but intensifying competitive pressure on Micron.

Investment Implications: First-day liquidity and volatility will be extreme. Long-term the stock benefits from dual drivers of US localization and the AI HBM supercycle; monitor its share battle with Micron.

2. Meta Platforms – Zuckerberg Denies Excess Compute Capacity and Advances Cloud Business

Event Overview: Zuckerberg explicitly denied the “excess compute” narrative, stating “I don’t know anyone in the industry who thinks they have excess compute,” and confirmed Meta is seriously considering leasing part of its AI infrastructure to external customers, noting a cloud business “definitely has commercial potential.” The company simultaneously launched the paid Muse Spark 1.1 model (its first enterprise-paid AI model) with aggressive API pricing (≈$1.25 per million input tokens, well below peers) and $20 free credits for new users. Zuckerberg highlighted strong performance on agentic tasks, coding, and tool-use benchmarks (e.g., MCP Atlas 88.1%) and criticized competitors’ “extreme” pricing. Earlier shareholder remarks had already indicated the cloud business was “definitely on the table,” with external firms inquiring almost weekly.

Market Interpretation: Institutions broadly view this as a pivotal shift for Meta from pure AI spending to potential high-margin cloud/API revenue. Multiple analysts believe aggressive pricing can capture developer share and create network effects similar to its advertising business. Denying overbuild while confirming cloud plans effectively eases concerns over $145 billion-scale capex. Near-term price elasticity is high; some banks have raised confidence in Meta’s AI monetization path, noting its advertising cash-flow advantage enables a price war.

Investment Implications: Successful cloud launch would reshape Meta’s valuation from “social + ads” to a diversified “AI infrastructure + models” story. Short-term catalysts are clear, but actual contract progress must be watched.

3. Micron Technology – US Investment Raised to Over $250 Billion by 2035

Event Overview: On July 9 Micron formally announced it will raise total US investment to more than $250 billion through 2035 (an increase of ≈$50 billion), targeting 40% of its DRAM production in the United States. The same day it held a first-concrete-pour ceremony at the Clay, New York mega-fab (the largest semiconductor manufacturing site in US history). The Idaho fab is expected to produce first wafers in mid-2027, with a second fab by late 2028. The New York project is projected to create 50,000 jobs (including 9,000 direct), with nationwide total exceeding 90,000. CEO Sanjay Mehrotra thanked President Trump, Secretary Lutnick and other officials, calling “data and memory the foundation of the modern economy,” and allocated up to an additional $3 billion for supply-chain strengthening.

Market Interpretation: Wall Street sees this as the most direct response to the CHIPS Act and Trump administration reshoring policy, as well as a preemptive move against Lutnick’s pressure on Korean firms. Institutions are broadly positive: capacity localization will significantly boost Micron’s global HBM and advanced DRAM share and profit stability while creating jobs and supply-chain security premium. Some analysts note large investment may temporarily pressure free cash flow, but under tight AI-driven supply it will convert into pricing power and valuation re-rating. Shares rose more than 4% on the day as the market rapidly priced in dual policy and demand catalysts.

Investment Implications: Long-term capacity and policy dividends are clear; near-term benefits from sentiment and sector rotation. Watch 2027 first-wafer delivery and HBM share trajectory.

4. Tesla – Optimus Gen3 Production Ramp Targets Issued

Event Overview: According to LatePost and multiple supply-chain sources, Tesla recently issued concrete Optimus Gen3 parts procurement guidelines requiring suppliers to reach 1,000 units/week capacity by September and 2,000–2,500 units/week by year-end (≈100,000 units annualized parts supply). Musk had already approved the latest Gen3 design in an executive meeting, marking the transition from lab to production after more than three years of RD. Suppliers have already seen hundreds of units of August orders roughly two months in advance. Fremont will lead initial production (slow at first); a dedicated Austin factory is under construction with long-term multi-million-unit plans.

Market Interpretation: Institutions and supply-chain analysts view this as the critical inflection from “concept demo” to genuine production delivery. Nomura and UBS had previously raised 2026 shipment forecasts (≈25,000 units); the hard targets further validate execution. The market interprets this as the start of meaningful robot revenue contribution (target price ≈$20,000 per unit), potentially becoming a new pillar that lifts TSLA’s valuation from “auto + energy” to “embodied AI.” Short-term supply-chain orders boost sentiment, though early yield and cost risks remain.

Investment Implications: The narrative-to-delivery inflection for robotics is approaching. Hitting September capacity targets would meaningfully raise the long-term valuation anchor; near-term volatility will still be influenced by auto deliveries and macro conditions.

5. Oracle – Credit Rating Downgraded to Lowest Investment Grade

Event Overview: On July 9 SP Global Ratings lowered Oracle’s long-term issuer credit rating from BBB to BBB- (lowest investment-grade notch) with a stable outlook. The main reasons are rising business risk and weaker cash flow from rapid AI infrastructure expansion: FY2027 capex is now projected at $90–95 billion (previously ≈$60 billion), with free operating cash flow deficit potentially widening to ≈$42 billion. Debt stands at ≈$160 billion and customer concentration (OpenAI, xAI, Meta, etc.) risk has increased. Despite this, Oracle still holds $638 billion in cloud contract backlog, and the stock rose on the day.

Market Interpretation: Institutional views are split. Rating agencies emphasize the structural hit of “AI burn” on traditional software giants’ financial flexibility and warn of high-leverage expansion vulnerability. Most buy-side analysts and banks, however, focus on the massive cloud backlog and AI infrastructure first-mover advantage, arguing near-term cash-flow pressure can be covered by long-term contracts and that the downgrade creates a buying opportunity. Some banks call this a classic pain point of AI-era “asset-heavy transformation,” which may appear at other traditional tech companies.

Investment Implications: Longer AI return cycles put rating and funding-cost pressure on high-leverage expanders. Watch FCF inflection and contract conversion rates; short-term volatility may offer structural opportunities.

IV. Cryptocurrency Project Updates (Past 24 Hours)

1、Bloomberg reported that Korean memory-chip maker SK Hynix completed its US ADR offering, raising $26.5 billion at $149 per ADR (177.9 million ADRs), becoming the third-largest IPO in US history. The price represented ≈3% premium to the Seoul close, with oversubscription exceeding 7x and nearly half taken by the top-10 order accounts. SK Hynix holds 57% global HBM market share. ADRs are expected to begin regular trading on July 13 amid the AI infrastructure boom.

2、CoinDesk reported that US spot Bitcoin ETFs recorded ≈$4 billion net outflows in June alone (led by BlackRock’s IBIT), with capital rotating toward AI trading and SpaceX IPO opportunities. Bitcoin fell ≈14% in Q2, recording its third consecutive quarterly loss. These outflows pale beside the $2 trillion private-credit market, where Q2 redemption requests hit $15.6 billion and 10 of 16 BDCs breached the 5% quarterly cap. Fitch expects continued pressure.

3、Sources indicate a unified version of the US Clarity Act may be released as early as next week, merging Senate Banking and Agriculture Committee work, with a full Senate vote targeted for the week of July 20.

4、Bitwise senior investment strategist Juan Leon stated that the current Bitcoin bear market is fundamentally different from prior cycles due to accelerating institutional adoption. Long-term holders view dips as “accumulation opportunities,” while larger capital still awaits clearer regulation. He called the ≈50% drawdown “the mildest structural bear market,” noting bottoms are rising each cycle.

5、Cathie Wood’s Ark Invest bought 217,896 shares of Circle (≈$13.7 million) on Thursday while selling 85,319 shares of Robinhood (≈$9.8 million).

V. Today’s Market Calendar

Data Release Schedule

| 00:00 | United States | WASDE Report | ⭐⭐⭐ |

| 01:00 | United States | Baker Hughes Oil/Total Rig Count | ⭐⭐ |

Key Event Preview

- SK Hynix Nasdaq listing begins trading: All day – key sentiment gauge for the memory sector

- US-Iran conflict follow-up statements and mediation progress: Anytime – source of oil and safe-haven volatility

Institutional Views

Over the past 24 hours, US tech and memory stocks led, oil pulled back, precious metals stayed range-bound, and crypto recovered modestly. Leading investment banks remain constructive but cautious: most believe the US-Iran conflict is a disturbance but does not alter the AI capex main theme; memory and compute names (MU, AMD, SK Hynix) benefit from dual policy and demand catalysts. Bank of America and others reiterate that Nvidia’s fundamentals have not reversed and its valuation discount is attractive. On oil, the consensus is more bearish short-term as the geopolitical premium fades. In crypto, institutions note that ETF outflows and liquidations remain controllable and BTC’s relative resilience indicates ongoing institutional allocation, though further macro data clarity is needed. Overall consensus: “Seek structural opportunities amid divergence” rather than a broad risk-on rebound.

Disclaimer: The above content is compiled by AI search and verified by humans for publication only. It does not constitute any investment advice. Data in the text inevitably contain deviations; please refer to real-time market data.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Why former Bank of America strategist sees an Ethereum ‘tactical bottom’

SWIFT Just Named 30+ Ripple (XRP) Connected Banks. Here’s why

Solana News: Santiment Flags Record Bearish Sentiment, Analyst Eyes $127

3 Altcoins That Could Reach All-Time Highs This Weekend, July 11-12