Nonfarm payrolls cool down, rate hike expectations fall, storage tests AI narrative

Show original

By:新全球资产配置

Bitget offers one-stop trading for cryptocurrencies, stocks, and gold. Trade now!

A welcome pack worth 6200 USDT for new users! Sign up now!

Performance and Valuation of Major Global Indices (USD denominated) and Valuation

Source: Bloomberg

Key Insights

Last week, U.S. June non-farm payrolls came in significantly weaker than expected, with only 57,000 new jobs added. The previous two months’ data was revised down by 74,000 jobs in total, and a decline in labor force participation also diminished the value of the drop in the unemployment rate. The employment data weakened the need for a short-term rate hike, leading funds to briefly rotate from high-growth AI sectors to interest-rate-sensitive traditional industries. The Dow hit another record high, and “Old Economy” Chinese stocks also saw a notable recovery. In the AI sector, recent market focus has been on rising storage prices and Meta’s plan to lease idle computing power. This reflects the new phase of AI capital expenditure, which emphasizes efficiency and returns, but does not signal the peak of the industry cycle. In the short term, stock price volatility is mainly driven by capital flow and sentiment shifts.

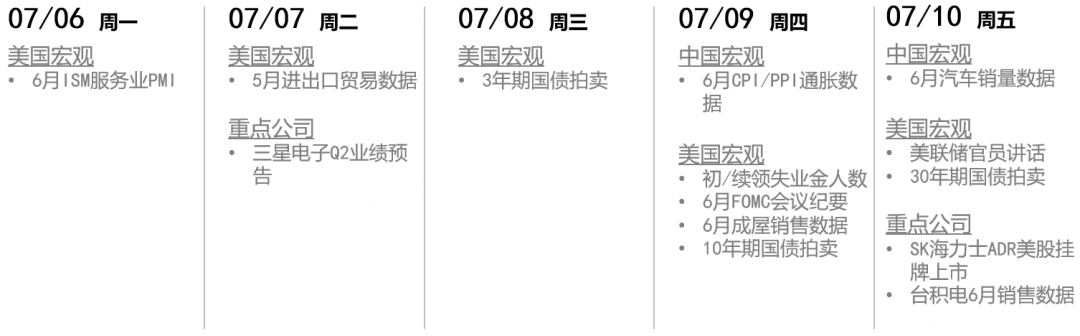

From a mid- to long-term perspective, as long as model vendor ARR continues to grow and AI Agent consistently brings cost reductions and efficiency improvements, the AI CAPEX theme remains intact. This week, pay close attention to Samsung’s Q2 earnings preview and SK Hynix’s ADR listing, as both will serve as tests for the storage industry trend and for crowding in the sector. However, whether the next phase of the rally can continue will depend on U.S. June CPI over the next two weeks and the earnings results of TSMC and ASML as proof points for computing power demand and equipment orders.

This Week’s Key Focus

U.S. Market & Greater China Market

Last week, the U.S. released the June non-farm payroll report, which was overall weaker than the previous narrative of “a stabilizing and improving job market.” Only 57,000 non-farm jobs were added, about half of market expectations, with the previous two months revised down by 74,000 in total; labor force participation fell from 61.8% to 61.5%. The decline in unemployment rate was more due to people leaving the labor force rather than a significant increase in hiring demand. By industry, the IT sector lost 9,000 jobs and leisure & hospitality lost 61,000, which were the main drags on employment this time. Meanwhile, average hourly wages ticked up year-over-year to 3.5%, with IT, finance, and professional services—high-wage sectors—remaining resilient, suggesting the labor market is not uniformly weak, but rather showing a “slowing in hiring, lower participation, and sticky wages” combination.For the market, this report weakens the necessity of a near-term rate hike, so funds rotated into non-AI traditional sectors that are sensitive to interest rates.As a result, the Dow posted a new record high and the “Old Economy” stocks in Greater China also saw a significant rebound.

Source: Bloomberg

Recently,there are two main AI trading focuses: rising storage prices and model vendors leasing idle computing power. Essentially, these both point to increased constraints on AI capital expenditure efficiency, but do not signify the peak of the investment cycle.The rise in storage prices is reshaping costs and profit distribution, pushing up cost pressure on consumer electronics and cloud vendors in the short term and forcing the industry to place more emphasis on investment returns. As new capacity comes online in 2027–2028, the storage sector is expected to shift from price expansion to volume growth, driving advanced storage and high-end packaging equipment demand. On the other hand, model vendors leasing out idle computing power is more a market mechanism to monetize low-utilization assets rather than a simple computing power surplus. In the short term, the decline in rental prices of last-generation chips and pressure on small and medium data centers may impact sentiment; in the mid-term, as long as model vendor ARR continues to grow and AI Agent continues to deliver cost reduction and efficiency, the AI CAPEX logic remains, only entering a new phase of joint validation by models, hardware, applications, and cash flow.

Looking ahead to this week, the market focus remains on the AI storage sector, with Samsung’s Q2 earnings preview and SK Hynix’s ADR listing in the U.S. set to be key events to test the strength of the storage—and even the entire semiconductor—rally. We believe that,compared to the financial numbers themselves, it’s more important this week to watch the trading pace after positive news has been realized.Despite a continued strong industry trend in the storage sector, positions are extremely crowded and expectations are highly unified. Thus, earnings and listing events may remain short-term profit-taking opportunities for capital. In the longer run, the next catalyst or inflection point for AI trades may come next week: the macro focus will be U.S. June CPI figures; in the industry, TSMC and ASML earnings will be key to confirming whether computing power demand continues to expand, advanced process capacity continues to scale, and semiconductor equipment orders remain robust—all of which are crucial for the next AI trade cycle.

0

0

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

Understand the market, then trade.

Bitget offers one-stop trading for cryptocurrencies, stocks, and gold.

Trade now!

You may also like

3 Altcoins That Could Reach All-Time Highs This Weekend, July 11-12

BeInCrypto•2026/07/10 17:51

Solana Ecosystem Metrics Support Recovery Setup

Cryptonewsland•2026/07/10 17:48

Ethena’s USDe deposits surge to $324M on Morpho in four weeks

Cryptobriefing•2026/07/10 17:39

Crypto prices

MoreBitcoin

BTC

$63,844.28

+1.23%

Ethereum

ETH

$1,788.52

+2.40%

Tether USDt

USDT

$0.9992

+0.01%

USDC

USDC

$0.9997

-0.00%

XRP

XRP

$1.1

+0.52%

Solana

SOL

$77.71

-0.39%

TRON

TRX

$0.3303

-0.47%

Hyperliquid

HYPE

$67.63

+0.53%

Dogecoin

DOGE

$0.07395

+1.38%

Zcash

ZEC

$500.1

+5.98%

How to buy BTC

Bitget lists BTC – Buy or sell BTC quickly on Bitget!

Trade now

Become a trader now?A welcome pack worth 6200 USDT for new users!

Sign up now