ServiceNow drops from 211 to 99: Why is a "work order selling" company still worth your attention?

I. From ServiceNow’s 50% Drop From Its Peak: What Really Happened?

If you held ServiceNow (NYSE: NOW) at the beginning of 2025, you probably wouldn’t feel like laughing right now—this leading enterprise software company hit a high of $211 in January 2025, but by April 2026, had crashed to a 52-week low of $81.24. Even after a recent rebound to $99–102, the stock is still about half its peak. On the surface, the reasons given by the market sound clear enough: AI will replace white-collar workers so fewer SaaS seats are needed, ServiceNow diluted its profit margins by acquiring Armis for $7.75 billion, and delays with major Middle Eastern contracts dragged down Q1 growth—each point enough to send a growth stock into the doghouse. But if you actually look at the financials, the story is not “the fundamentals collapsed.” In FY2026 Q1, ServiceNow’s total revenue was $3.77 billion, up 22.1% year-over-year, subscription revenue was $3.671 billion, up 22%, cRPO (next 12 months' revenue under contract) was $12.64 billion, up 22.5%, and RPO (total backlog) reached $27.7 billion, growing 25%. In other words, the “future workload” sold to customers wasn’t declining, but accelerating. Now Assist customers with annual contract value over $1 million increased by 130% YoY. The reality is this: the market isn’t pricing ServiceNow’s fundamentals, but rather the “will AI put it out of business” narrative anxiety, and has gone overboard. When a company growing 20%+, with 35%+ free cash flow margins, and a net cash balance sheet, gets pressed into trading at 19–23x forward PE and a PEG near 0.88–1, it’s not just a “software stock” anymore, but a question of pricing deviation.

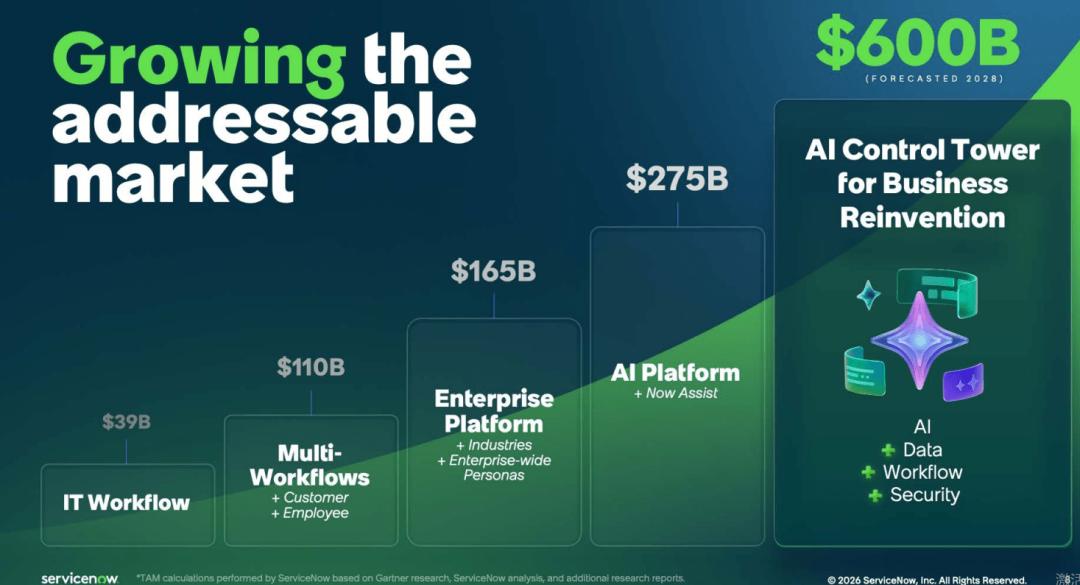

Chart below:ServiceNow's TAM will reach $600 billion by 2028

II. It's Not Just a “Ticket System,” but the Central Nervous System of the Enterprise

Many people still see ServiceNow as the “system IT departments use to issue work orders”—password resets, fixing hardware, onboarding/offboarding workflows—but that’s not the core today. More accurately, over the past 20 years, ServiceNow has built, within the tech stacks of the world’s largest enterprises, the only “system of record” and “single data model”: no matter what department you’re from, which cloud you use, or what legacy ERP you run, if it involves who requested what, who approved something, what configuration was changed, and which assets are affected, that process ultimately lands in ServiceNow’s CMDB (Configuration Management Database) and context engine. Its moat isn’t some flashy AI feature, but switching costs—replacing it would be like ripping out and reattaching the very backbone of “who did what, who has what rights, and how to audit” for the whole company—nobody dares. Now, on this base, ServiceNow has repositioned itself as the so-called “AI Control Tower”—meaning: AI agents can reason anywhere, but to actually take action within the enterprise (change config, grant permissions, adjust supply chain, provision laptops), they must go through an orchestration layer with permissions, audit trails, rollback, and zero-trust access. The infrastructure ServiceNow spent 20 years building is exactly this orchestration backbone, and the AI era happens to make “who controls what actions” a matter of business survival, not just compliance. Nvidia’s Jensen Huang publicly called it the “AI Operating System for Enterprises,” and said Nvidia itself uses ServiceNow—this is not a casual plug. When the CEO of the world’s biggest AI compute company endorses your “orchestration layer,” he’s actually reducing cognitive friction for all CIOs: want to roll out Agentic AI? First, ask who’s in charge.

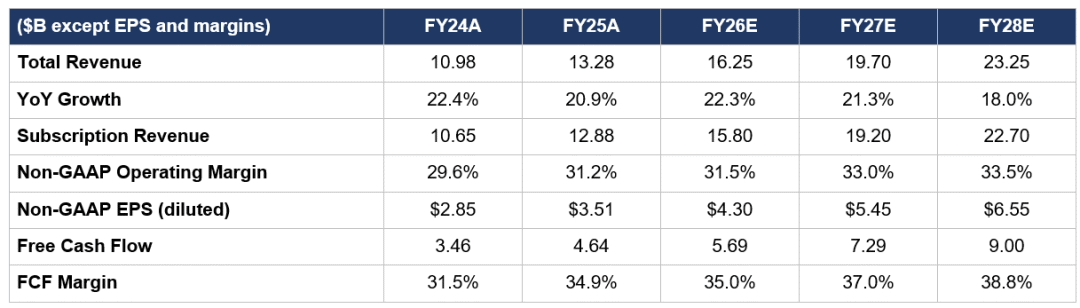

Chart below: NOW financial overview

III. AI Agents Arrive: Not Only Was ServiceNow Not Eaten, It Started “Collecting Tolls”

One of the most common bear narratives is: AI agents will replace human workers, fewer humans means fewer ServiceNow SaaS seats, so it cannibalizes itself. Sounds logical, but the actual math says the opposite. ServiceNow is already shifting pricing from “per seat” to a “hybrid” (subscription + consumption) model—about half of new business now comes from non-seat pricing. Here’s how you can look at it: previously a 20-person IT support team would cost around $1 million a year ($900k for salaries, $20k for ServiceNow licenses). Now, ServiceNow’s autonomous agents take the work of 15 of those 20, and the customer needs only 5 staff. It looks like “15 seats gone,” right? But the labor costs saved on those 15 staff largely convert into AI agent token consumption—ServiceNow calls these “Assist” tokens. In this case, even after losing those 15 human seat licenses, ServiceNow’s actual billing from that workflow expands over fivefold, because the agent consumption is about 6.5x the seat license. This isn’t just theoretical—the Q1 data already shows early signals: Now Assist $1m+ ACV clients grew 130% YoY, total Now Assist consumption in Q1 hit $750 million, with a full-year goal of $1.5 billion. And at the 2026 Knowledge conference, the launch of Action Fabric plus MCP (Model Context Protocol) integration allows third-party AI agents—whether Microsoft Copilot, Google Gemini, or Anthropic’s Claude—to use ServiceNow’s context engine and CMDB to “plug in” safely for execution. For example, if a user asks Copilot to provision a laptop or change a supply chain order, Copilot must route that action via Action Fabric, burning an Assist token every time. In simple terms: ServiceNow doesn’t compete with Microsoft/Google over whose model is smarter; it fights to make sure all models entering the enterprise must go through its checkpoint, where it takes a cut. This is the real meaning of “collecting tolls” and is its ace against LLM commoditization.

IV. A $12 Billion M&A Bet: They’re Buying Not Revenue, but the “Active Directory” of the AI Era

In the past 12 months, ServiceNow closed deals for Moveworks (~$2.4B), Logik.io (~$500M), Veza (~$1.25B), and Armis ($7.75B)—around $12B in “external tech stacks” to be integrated into a foundation built organically. Wall Street’s first reaction was understandable: margin dilution panic—Armis alone drops FY26 operating margin by 50–75bps, FCF margin by about 200bps. The share price tanked first. But why spend this money? The answer is in the “non-human identity” time bomb that almost no one seriously manages. By 2030, enterprises will have more AI agents than human employees, and many of those agents—often with high-level permissions—are “shadow identities,” without continuous monitoring of what they can/cannot touch or when they cross boundaries. Veza brings patented Access Graph tech, mapping every human, machine, and AI identity’s permission paths across all systems; Armis brings panoramic, agentless, real-time discovery of IT, OT, IoT, medical, and even “physical AI,” tracking about 6.7 billion devices. Feeding Veza (identity) and Armis (asset) into ServiceNow’s Context Engine and AI Control Tower means it isn’t just a “ticketing system” anymore—it’s the only one that can see “which shadow AI agent is touching what it shouldn’t” in milliseconds and auto-shut it down. ServiceNow says the Armis deal triples its TAM in security and risk solutions. Translated for investors: it spent $12B buying a ticket to “enterprise AI zero-trust infrastructure,” not for boosting quarterly growth rates.

V. The Middle East's Deferred Accounting Drama—An “One-Off Pre-Booked Revenue” Spring Wrapped in Bad News

The post-Q1 earnings selloff, beyond M&A dilution worries, was also triggered by management saying subscription growth hit a 75bps headwind due to delayed deals in the Middle East. It sounds scary, but the mechanics matter—the Middle East business is “sovereign cloud” deployments, and under ASC 606 revenue recognition, these on-prem deals aren’t recognized monthly but upfront once the contract is finalized. So “delayed” isn’t “lost,” nor “taken by competitors”—management’s relationships with Middle East clients are intact, the pause is about geopolitics, not product competitiveness. Once these contracts sign in Q2 or Q3, a large upfront revenue recognition hits, directly offsetting the prior suppressed growth. In other words, the Middle East deferral is a psychological negative, but in financial terms it’s a compressed spring. This market punishment (from $211 down to $81) far exceeds the real weight of this headwind—and when you realize cRPO is still growing 22.5% YoY, it’s clear that those 75bps are “visible noise,” not a broken trend.

VI. Numbers Don’t Lie: A High-Quality Compounder Trading at PEG Below 1, Target Price Calculation

Let's lay out the valuation simply. ServiceNow trades at $99–102, with a forward P/E around 19–23x (platform consensus aggregates differ), with subscription growth still at about 20%, FCF margin steady around 35%, 98% gross retention, and ~$11B net cash on the balance sheet. Q1 operating cash flow was $1.67B, FCF $1.665B. PEG computes to roughly 0.88–1.0—meaning you pay a P/E almost equal to (or even below) its earnings growth rate, rare for high-quality enterprise software. For context: Microsoft at 12% growth trades at over 30x forward PE (PEG ~2.7), Palo Alto at 14% at over 40x (PEG 3+), Adobe growing single digits trades at just above PEG 1—while a 20% growth, 35% FCF Margin, net cash, 98% retention platform is at under 20x consensus FY27 EPS of ~$5.45? Either the market’s pricing in an unseen fundamental collapse, or it’s pricing an extreme “AI will replace ServiceNow” scenario that even it does not believe.

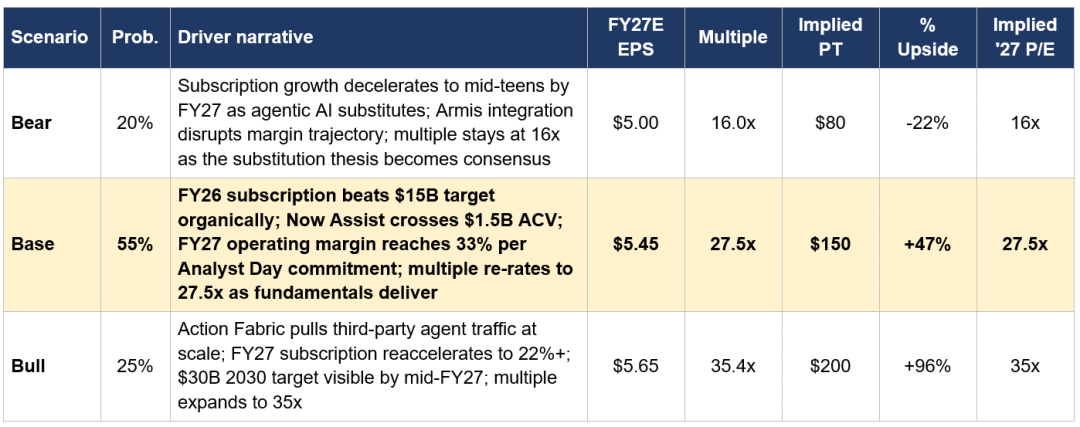

My base case model anchors FY27 non-GAAP EPS at ~$5.45 with a 27.5x forward PE (slight premium to peer median 23x but well below its 5-year average), giving a target price around $150; DCF with ~9.7% WACC/3% terminal growth cross-checks at ~$151. Probability weighted (bull/base/bear) lands at around $148—that’s about 46% upside from $99–102. Even with no fancy DCF, just mean reversion: it spent most of the last five years at a 40–60x forward PE premium, now crushed below 20x with the business intact—that's the source of the asymmetry.

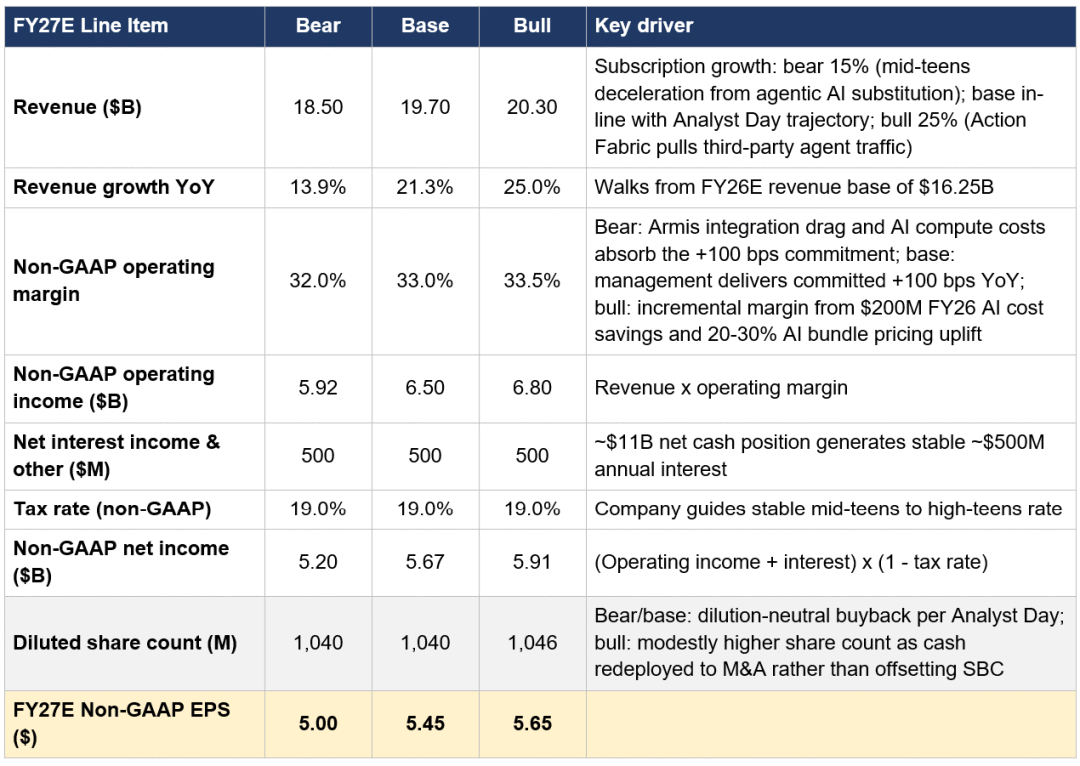

Chart below:Financial forecast scenario analysis table

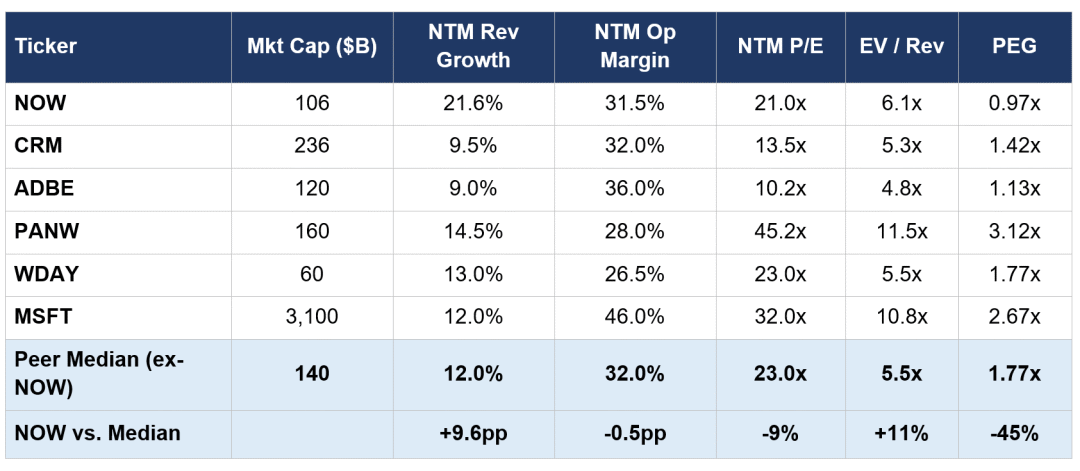

Chart below: Sector comparison

VII. Three Real Risks You Can’t Ignore

Of course, I’m not just bullish. The first risk is highly tangible: ServiceNow's 20-year valuation premium was built on that “single data model, single codebase” clean architecture, but now they need to integrate $12B worth of acquired tech—Armis asset management, Veza's identity graph, Moveworks' conversational front-end—an engineering challenge that costs real money. The FY26 75bps operating and 200bps FCF margin drag is the price of this complexity. If integration drags into 2027 without converging, the market will price in a “more complex/slower” discount. The second risk is “bypassing the built-in guardrails”—some big customers are trying to plug in their own security stacks (e.g. Palo Alto’s Protect AI) instead of going all-in on ServiceNow’s native Now Assist Guardian. If major clients split “ServiceNow for workflow, others for security,” ServiceNow just becomes a nice logging dashboard, not a high-premium business platform. Third is orchestration layer competition—if Microsoft convinces CIOs that “Azure/M365 is your local execution layer” using Copilot Studio, while Salesforce’s Agentforce (reportedly over $540M revenue) also competes for orchestration, then Action Fabric may face the awkwardness of “everyone says they’ll integrate but the traffic doesn’t come.” These are not low-probability risks, but they are the type that will be proven right or wrong within “the next two years”: as long as the next two clean quarters (Q2, Q3 FY2026) don’t see further profit margin cuts and there’s no mass client delay for Armis integration, the debate will quickly shift to the bulls’ favor.

VIII. Target Price & Strategy: What You Need Isn't a Prediction, but an Executable Framework

In summary, I currently rate ServiceNow as a strong BUY, but recommend a “phased + data-driven” strategy, not an all-in bet on a rebound. My pricing center is at $148–150 (about 46% upside)—this does not require a return to the historical 50x PE miracle, but simply market recognition that for a platform growing 20%+, with 35%+ FCF margin, net cash, and 98% retention, a 19x forward PE is mispriced. Just keep an eye on the next two validation windows: 1) whether Q2/Q3 subscription growth holds above 20%, Now Assist ACV makes stable progress toward the $1.5B annual goal, and $5M+ deal net adds don’t drop; 2) whether Middle East sovereign cloud contracts sign and recognize revenue—when the 75bps headwind reverses. Management is both issuing $4B in long-term debt to lock in low-cost capital and has $4.2B in repurchase authorization to buy shares near $99 (they already used $2B in Q1 for accelerated repurchases at $107.97 for ~18.5M shares), showing with the balance sheet that they think the price is disconnected from fundamentals. And as for the Trump stock angle—that’s irrelevant. What matters is: ServiceNow is evolving from “selling seats” to “collecting tolls from all enterprise AI agents,” and once the CIO community recognizes this role, a return to a 25–28x multiple ($130–150 target) is more of a timing issue, not a matter of faith.

Chart below: Target price calculation

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Altcoins That Could Reach All-Time Highs This Weekend, July 11-12

Solana Ecosystem Metrics Support Recovery Setup

Ethena’s USDe deposits surge to $324M on Morpho in four weeks