AI craze masks warning signs! Wall Street warns: if the 'double bubble' bursts, it may trigger the next big crash

FX168 Finance News Agency (Asia-Pacific) reported that if you ask a bullish stock market investor why they believe the current stock market is not in a bubble, the forward price-to-earnings ratio (Forward P/E Ratio) will almost certainly be one of the three reasons they list.

(Screenshot source: MarketWatch)

Artificial Intelligence (AI) enthusiasm has fueled a rapid rise in the stock market. However, despite major indexes such as the S&P 500 hitting new highs repeatedly this year, one of the most popular metrics used by fundamental analysts shows that stock valuations are actually becoming more attractive, rather than the opposite.

The reason is that analysts typically compare stock prices with the earnings per share that a company is expected to achieve over the next 12 months. While stock prices have risen sharply recently, Wall Street's expectations for earnings growth are increasing at an even faster pace.

According to Dow Jones market data, the S&P 500's forward P/E ratio was 22.4 a year ago. As of last Thursday's close (the latest data), this figure had dropped to 20.51—even though the S&P 500 index itself rose 20% over the same period.

As the second quarter earnings season approaches, the market expects S&P 500 component companies to achieve double-digit profit growth for the seventh consecutive quarter. According to FactSet data, analysts currently predict an overall earnings growth rate of more than 23% for these companies.

However, it remains unknown how long companies can maintain this pace of growth.

Panmure Liberum analysts Joachim Klement and Francisca Reis pointed out in a report submitted to MarketWatch that although current stock valuations remain extremely high compared to historical levels, the recent rate of earnings growth has also clearly deviated from long-term trends.

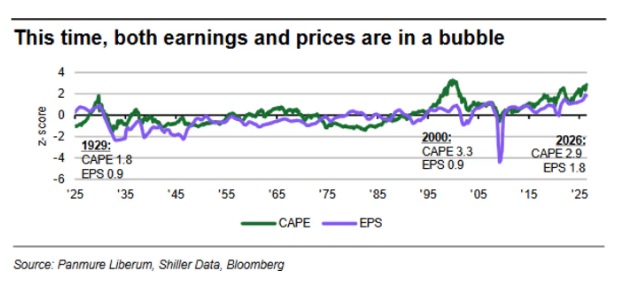

According to the analysts, using another widely watched valuation metric—the Shiller CAPE Ratio (cyclically adjusted price-to-earnings ratio)—the current S&P 500 valuation is about 41 times earnings, already close to the all-time highs set during the dot-com bubble 25 years ago.

However, there are significant differences between current profitability and that during the dot-com bubble era.

Panmure analysts noted that corporate earnings growth during the dot-com bubble was relatively mild, while today the S&P 500’s per-share earnings growth is already 1.8 standard deviations above the long-term trend line.

If the recent abnormally strong earnings growth is adjusted to a more normal level, the Shiller CAPE valuation for the S&P 500 would soar to 67.6 times, equivalent to 4.6 standard deviations above the long-term trend.

(Screenshot source: MarketWatch)

The analysts wrote that this level would exceed the peaks of every other asset bubble in U.S. history.

They further pointed out that, in other words, the current market might not just be a “price bubble,” but is close to a much more dangerous state—a “price bubble built on an earnings bubble.”

In a Financial Times column, Klement warned that “extraordinary” profits are unlikely to last; eventually, investors will have to face financial reality. Admittedly, corporate earnings could still continue to surge in the next few years. He noted that such growth momentum often lasts longer than investors expect.

However, as tech giants like Microsoft, Google parent company Alphabet, Amazon, Meta, and Oracle (referred to as “hyperscale cloud computing companies”) continue to invest heavily in building AI data centers, the likelihood of a return of corporate earnings growth to normal levels is increasing.

The reason is that these companies are shifting from the previous “asset-light model” to an “asset-heavy model,” constantly increasing capital expenditures, with the profitability model also set to change.

Klement and Reis are not the only analysts warning that earnings expectations may be overly optimistic.

Peter Berezin, Chief Strategist at BCA Research, pointed out that earnings bubbles have appeared many times in history. Before the global financial crisis of 2007-2008, the banking and real estate development sectors experienced similar circumstances. At that time, seemingly low P/E ratios concealed unsustainable profit growth.

Berezin wrote in a late-May report, “More broadly, earnings bubbles frequently occur in sectors with boom-bust cycles. These sectors include natural resources, aviation, shipping, and especially relevant in the current environment, the semiconductor industry.”

He indicated that Wall Street analysts often find it difficult to accurately predict when the earnings bubble will peak. Once the inflection point arrives, the stock market could fall by 30% to 50%.

(Screenshot source: MarketWatch)

Looking ahead, Andy Costan, CEO of Damped Spring Advisors, said in the program Monetary Matters in May that U.S. economic growth is insufficient to support the level of earnings currently expected by Wall Street.

Jim Paulsen, a Wall Street veteran, also recently stated that he believes the market’s optimistic expectations for corporate earnings are risky.

U.S. stocks experienced some turbulence in June, which extended into early July. The powerful momentum trading surrounding semiconductor stocks—a key driver of the market’s rise—showed signs of slowing.

However, semiconductor stocks rose again on Monday, lifting the Nasdaq Composite Index by 1.1%.

According to FactSet data, the S&P 500 index finished less than 1% away from its record high, while the Dow Jones Industrial Average closed above 53,000 for the first time, setting a new record.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

3 Altcoins That Could Reach All-Time Highs This Weekend, July 11-12

Solana Ecosystem Metrics Support Recovery Setup

Ethena’s USDe deposits surge to $324M on Morpho in four weeks